|

Audit,

Risk and Improvement Committee Meeting

Business Paper Business Paper

|

|

Noticeis

hereby given that an Audit, Risk and Improvement Committee Meeting of Parkes

Shire Council will be held in the Parkes Council Chamber, 2 Cecile Street, Parkes,

on Friday 13 October 2023 at 1:00pm.

|

|

|

|

Kent Boyd PSM

General Manager

|

|

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

The Chairperson will declare

the meeting open.

Meeting of Council

committees are not recorded or streamed to the internet.

2 Acknowledgement

of Country

Parkes Shire Council

acknowledges the Wiradjuri People who are the Traditional Custodians of the

Land. I would also like to pay respect to the Elders past, present and emerging

of the Wiradjuri Nation and extend that respect to other Aboriginal peoples from

other nations who are present.

3 Apologies

In accordance with clauses

5.3, 5.4 and 5.5 of Council's Code of Meeting Practice, apologies must be

received and accepted from absent Councillors and a leave of absence from the

Council Meeting may be granted.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

4 Confirmation

of Minutes

IP&R

Linkage: Pillar: Leadership

Goal: Our

local government is open, accountable and transparent.

Strategy: Provide open

and transparent decision-making and undertake the civic duties of Council with

professionalism and integrity.

Annexures: A. Audit,

Risk and Improvement Committee Meeting Minutes - 30 August 2023

|

Recommendation

That the receive and

confirm the Minutes of the meeting held on Wednesday 30 August 2023 appended

at Annexure A.

|

|

Audit,

Risk and Improvement Committee Meeting

Minutes

Wednesday 30

August 2023

|

|

|

|

|

|

Audit, Risk and Improvement

Committee Meeting Minutes

30 August 2023

|

Minutes

of the Audit, Risk and Improvement Committee Meeting

Held

on Wednesday, 30 August 2023 via

Microsoft

Teams

Present:

Mr Stephen Horne Chairperson

Mr Tony Harb Member

Dr Meredith Caelli Member

Cr Jacob Cass Councillor

(non-voting)

Cr Marg Applebee Councillor

(Alternate, non-voting)

Council Officers in Attendance:

Mr Kent Boyd General

Manager

Mr Anthony McGrath Director

Customer, Corporate Services and Economy

Mr Jaco Barnard Chief

Financial Officer

Mrs Mikaela Cass Manager

Governance, Risk and Corporate Performance

Mr Luke Nash Financial

Accountant

Miss Georgia Smith Business

Services Trainee (Minutes Secretary)

Guests

Mr Paul Quealey Lambourne

Partners (Internal Auditor)

NOTES

Councillor's Cass and Applebee attended via audio-visual

link.

The meeting commenced at 9.05am and concluded at 10.00am.

|

Audit, Risk and Improvement

Committee Meeting Minutes

30 August 2023

|

Order Of Business

1 Opening

of Meeting.. 4

2 Acknowledgement

of Country.. 4

3 Apologies.. 4

4 Confirmation

of Minutes.. 4

4.1 Minutes

of the Audit, Risk and Improvement Committee Meeting held on 27 July 2023. 4

5 Disclosures

of Interests.. 4

6 Late

Business.. 4

7 Officers'

Reports.. 5

7.1 Audited

Financial Statements for the year ended 30 June 2023. 5

8 Report

of Confidential Resolutions.. 6

9 Conclusion

of Meeting.. 6

|

Audit, Risk and Improvement

Committee Meeting Minutes

30 August 2023

|

1 Opening

of Meeting

The Chairperson declared the

Audit, Risk and Improvement Committee Meeting of Wednesday, 30 August 2023 open

and welcomed Council Officials in attendance.

2 Acknowledgement

of Country

The Chairperson read the

following Acknowledgement of Country:

Parkes Shire Council

acknowledges the Traditional Custodians of the Wiradjuri Country

and recognises and respects their cultural heritage, beliefs and continuing

connection with

the lands and rivers of the Parkes Shire.

Council pays its respects to

Elders past, present and emerging and extends this respect to

all First Nations peoples in the Parkes Shire.

3 Apologies

Leanne Smith - INTENTUS Chartered Accountants.

4 Confirmation

of Minutes

5 Disclosures

of Interests

The Chairperson reminded Council Officials of their

obligation under Council's Code of Conduct to disclose and manage any conflicts

of interest they may have in matters being considered at the meeting, and

invited Council Officials present to disclose any such interests.

6 Late

Business

The Chairperson advised that no late items of business had

been submitted to the meeting.

7 Officers'

Reports

|

7.1 Audited

Financial Statements for the year ended 30 June 2023

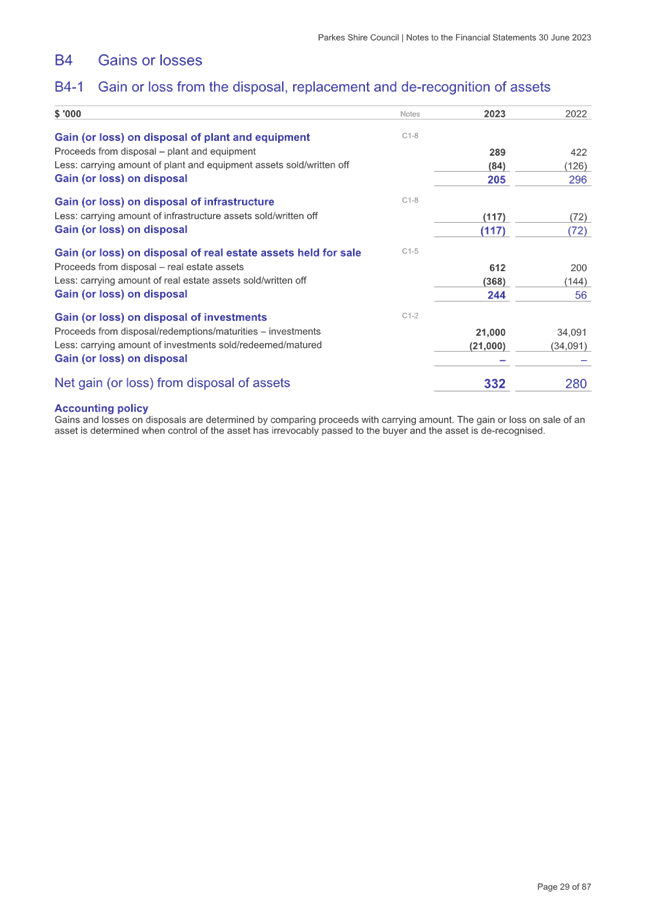

SUMMARY:

The Statements are a requirement of

Section 413(2) of the Local Government Act 1993 (as amended) and the Local

Government Code of Accounting Practice and Financial Reporting and form part

of the Annual Financial reports.

In order to comply with Section

413(2) of the Local Government Act 1993 (as amended) and the Local Government

Code of Accounting Practice and Financial Reporting, Council must prepare a

statement on the General-Purpose Financial Statement (GPFS) and the Special

Schedules as well as the Special Purpose Financial Statements (SPFS). The

Statement then allows the accounts to be referred for audit.

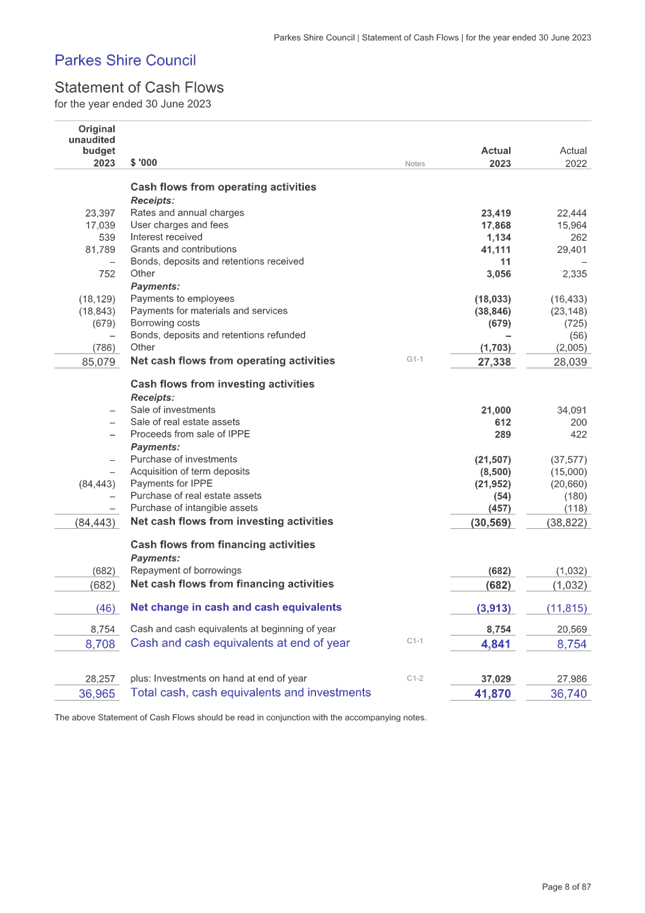

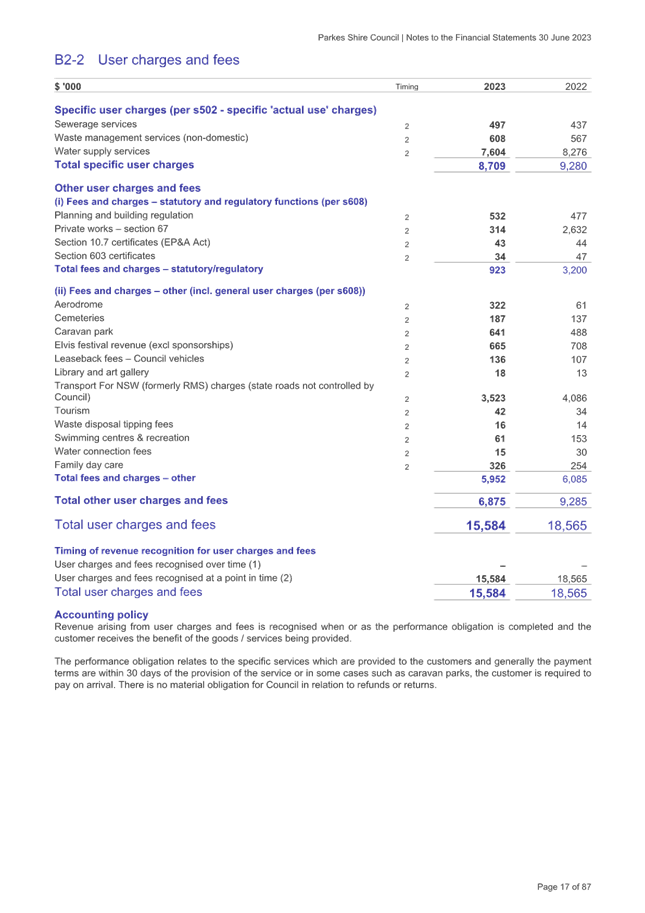

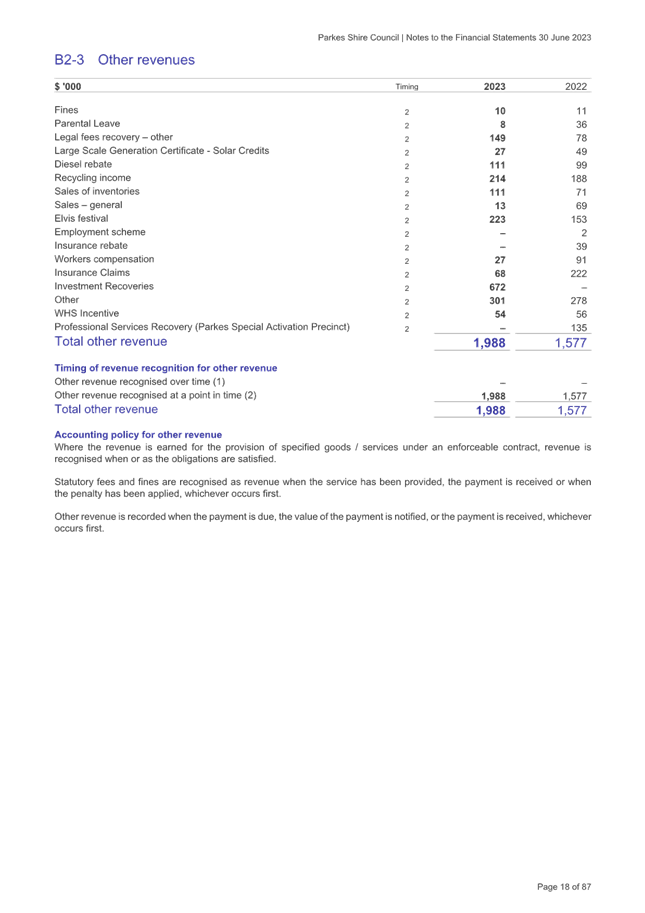

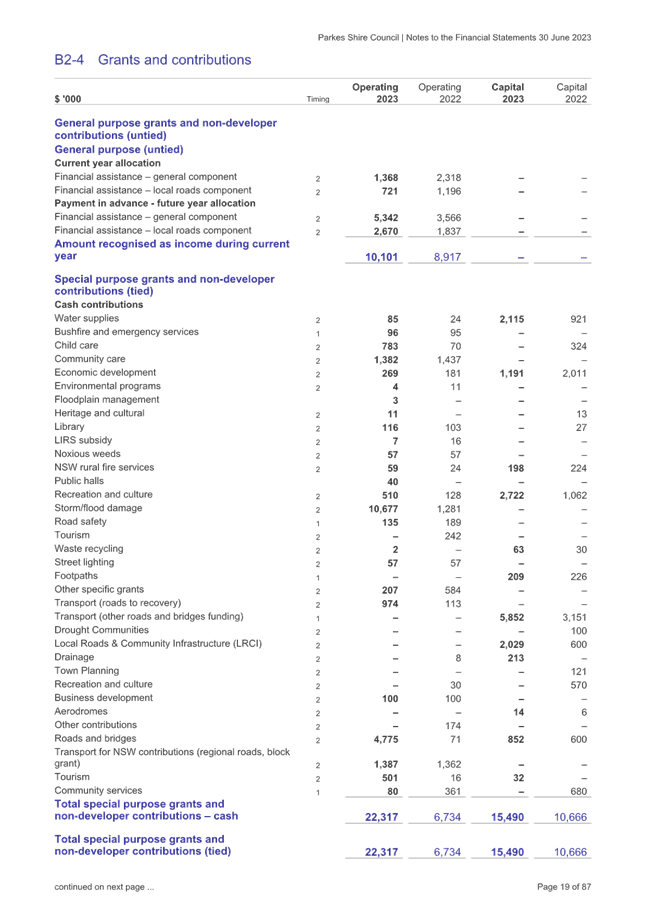

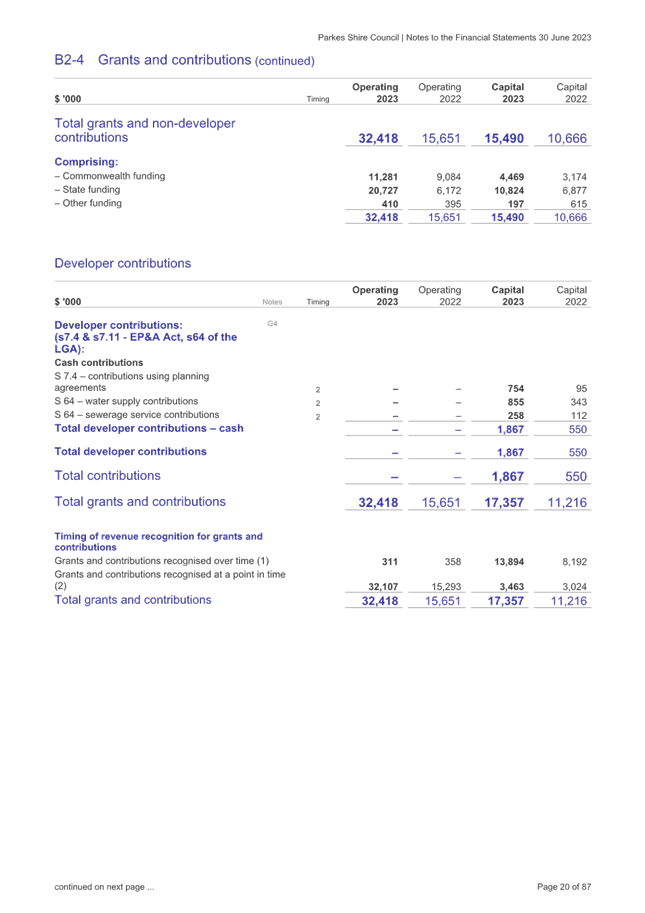

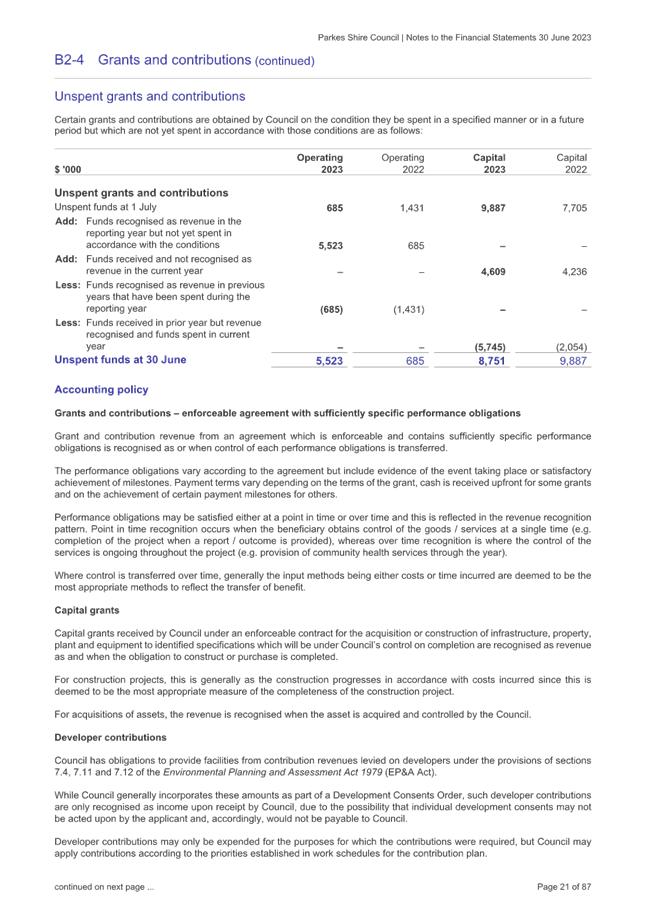

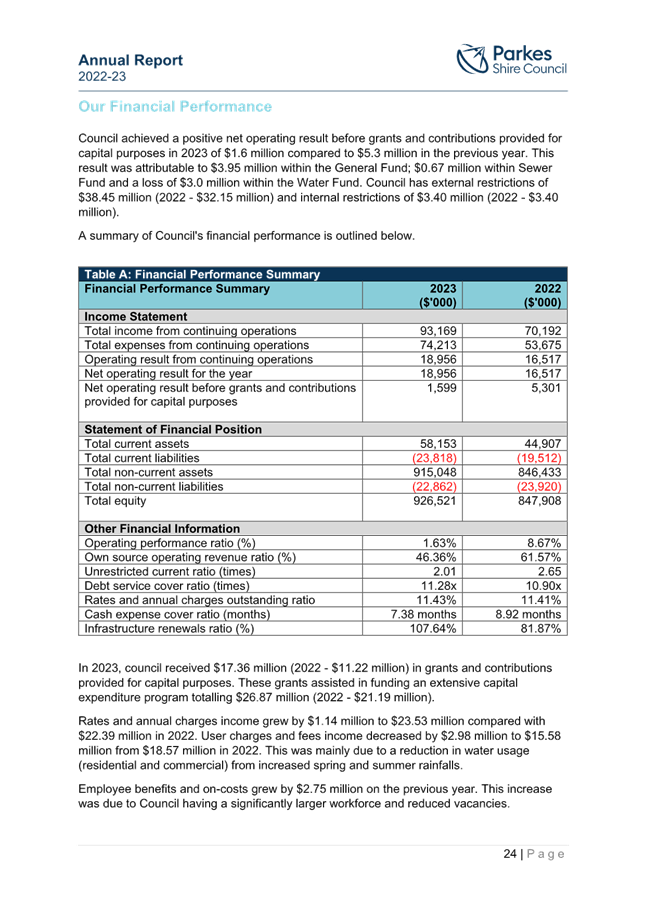

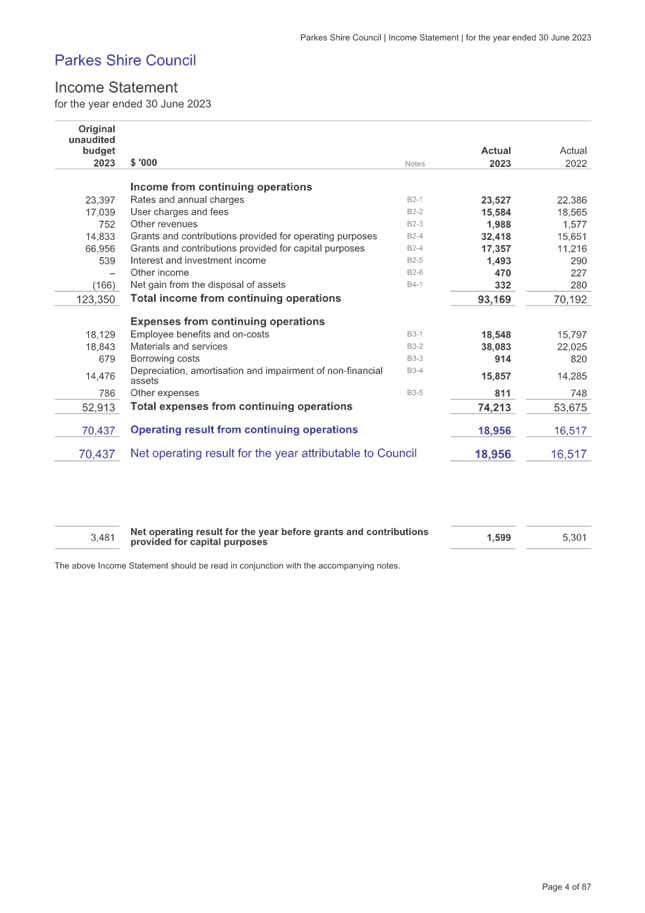

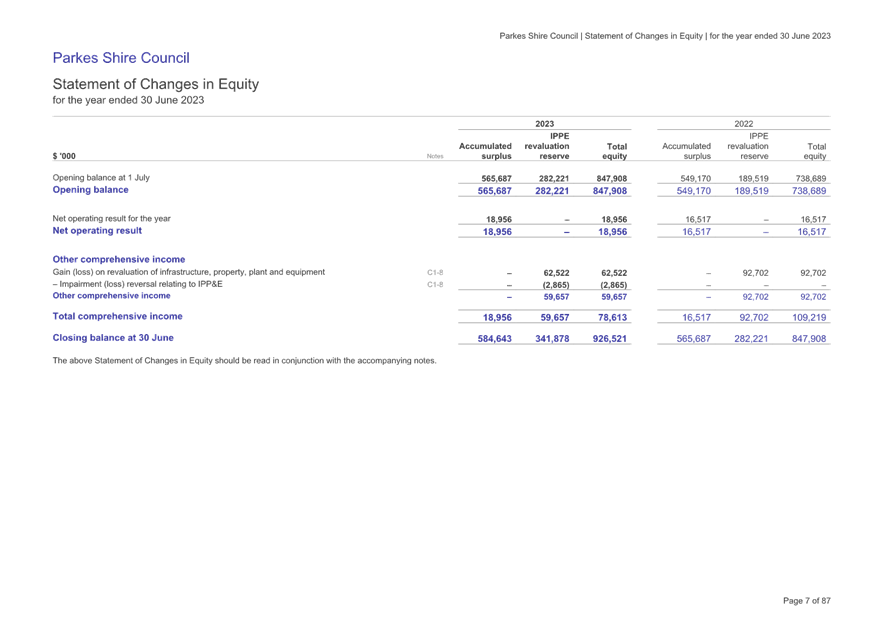

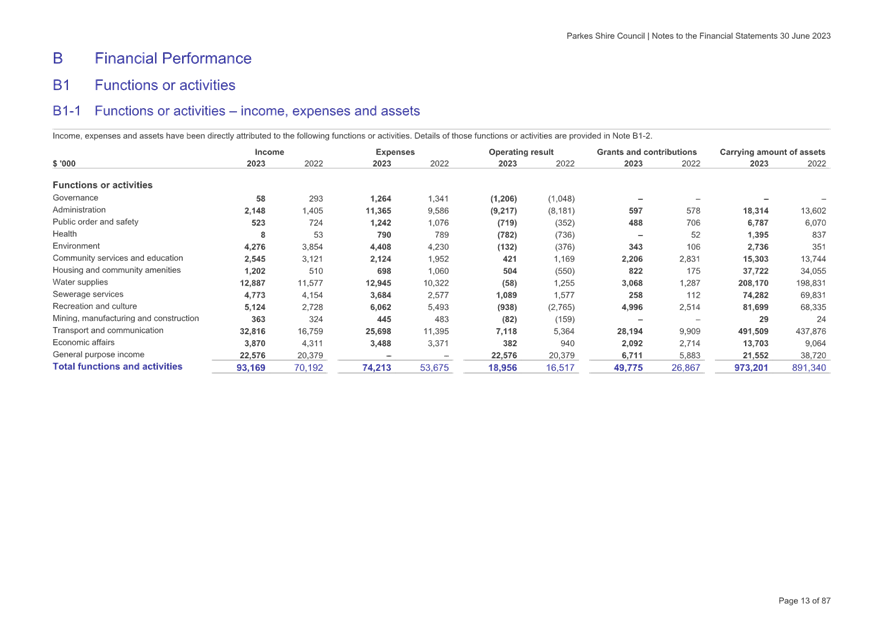

Council has recorded a financial

result in 2023 of $1,599,000 (subject to change during audit, details below)

for the year as compared to $5,301,000 in 2022. Several factors have enabled

council to achieve a positive operating result including increased grants and

contributions for operating purposes, interest income and other revenues.

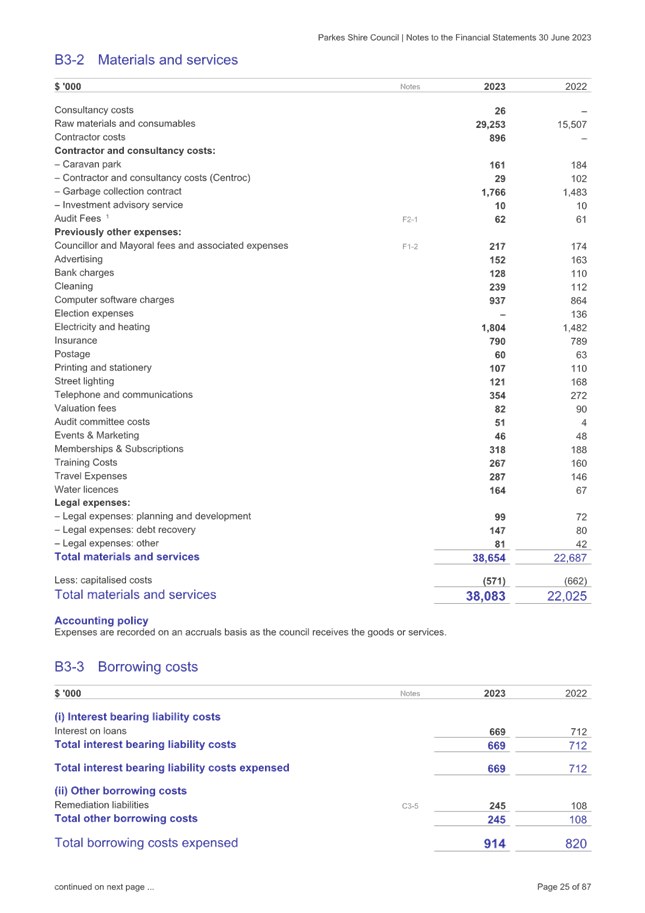

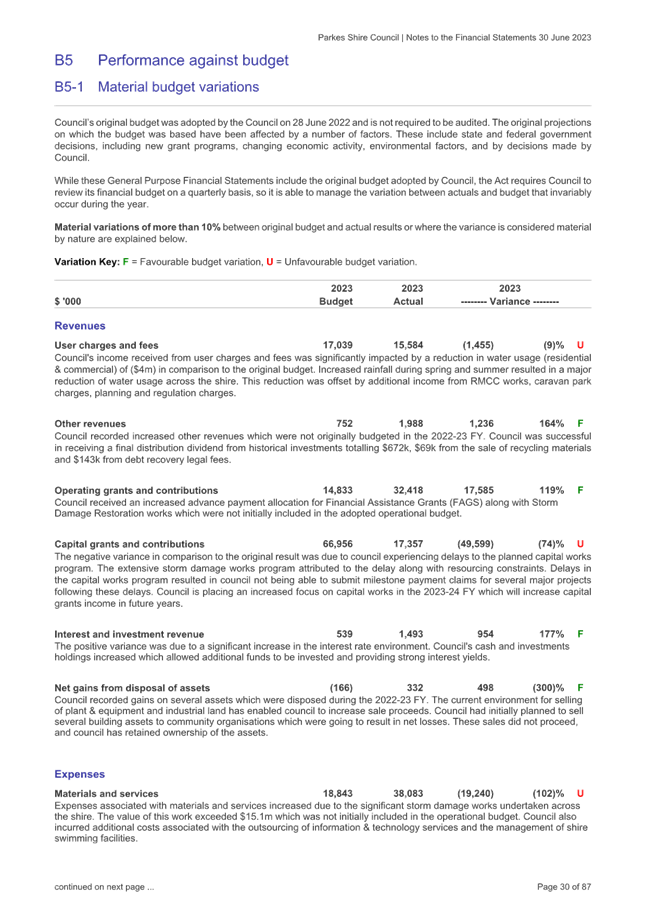

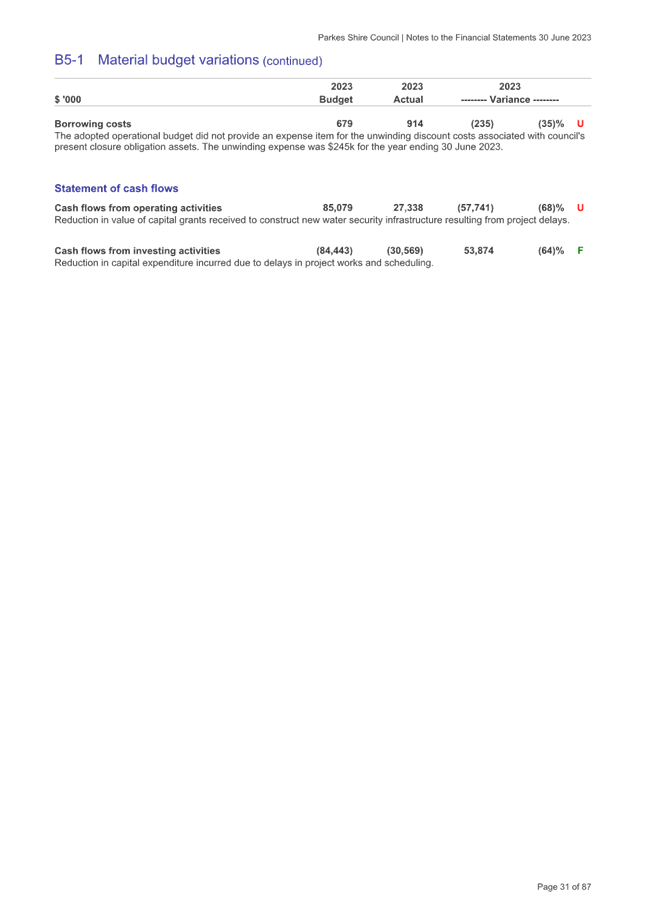

DISCUSSION:

The Committee discussed the

following:

·

The Committee congratulated the

Finance team on the work put in to put together the Financial

Statements.

·

The Chief Financial Officer spoke to

the report and informed the Committee of the following:

o

The $2.9 million loss in Council's

Water Fund won't be repeated in future years due to restructure of water

charges.

·

The Committee queried the following

in relation to the Income Statement:

o

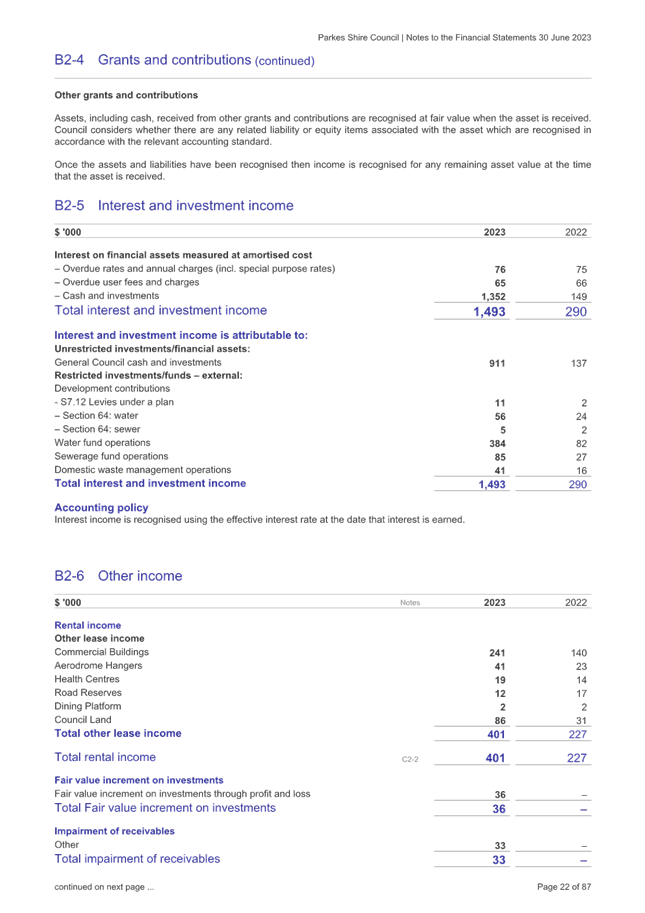

Increase in Interest and investment

income from 2022 to 2023. The Chief Financial Officer advised that this was

due to increased interest rates.

o

Increase in Materials and services.

The Chief Financial Officer advised that this was due to the increase in

costs of materials and works associated with storm damages, as well as

outsourced services such as the pools and ICT.

o

Variances of grants and contributions

compared to budget. The Chief Financial Officer advised that this relates to

the Safe and Secure Pipeline Duplication Project as the funds were budgeted

for, but not yet received.

·

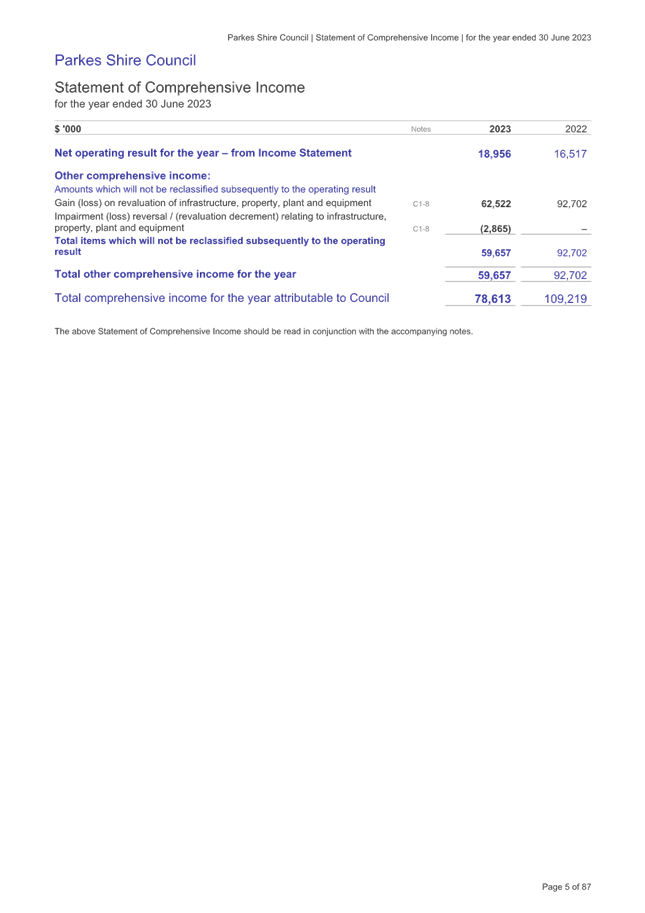

The Committee queried the following

in relation to the Statement of Comprehensive Income:

o

Increase in gain on revaluation of

infrastructure, property, plant and equipment. The Chief Financial Officer

advised that the increase relates to the indexation of asset categories and

revaluation of community land and buildings.

·

The Committee queried the following

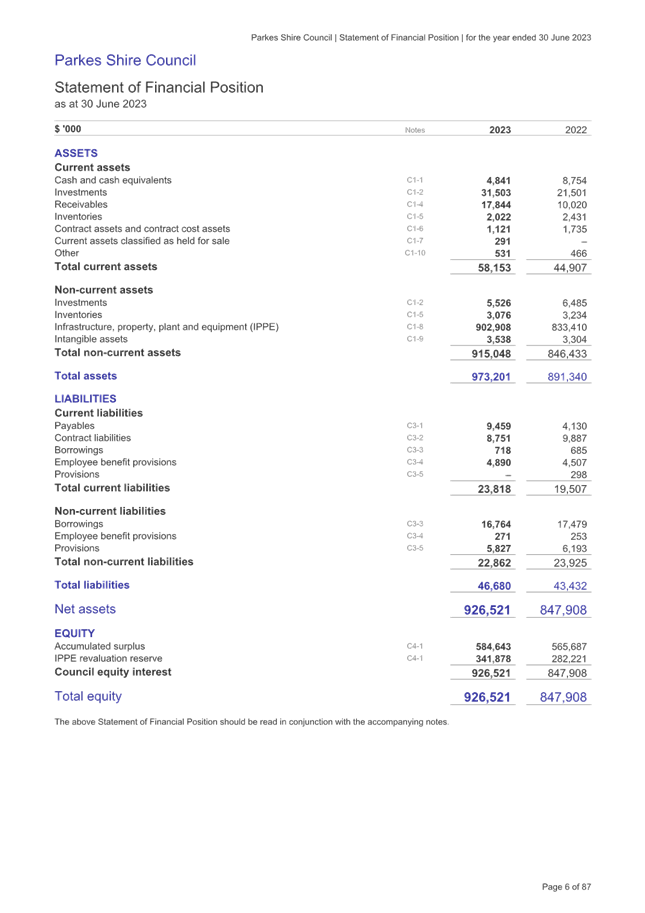

in relation to the Statement of Financial Position:

o

Increase in Receivables for the 2023 financial

year. The Chief Financial Officer advised that this is due to unspent funds

due to storm damages.

·

The Committee queried the process in

place to determine the Grant funding that Council applies for. The Chief

Financial Officer advised that Council utilises the Capital Plan when

applying for grants and Council's Executive Leadership Team (ELT) determine

whether Council has the capability to deliver these projects utilising grant

funds within a two-year period.

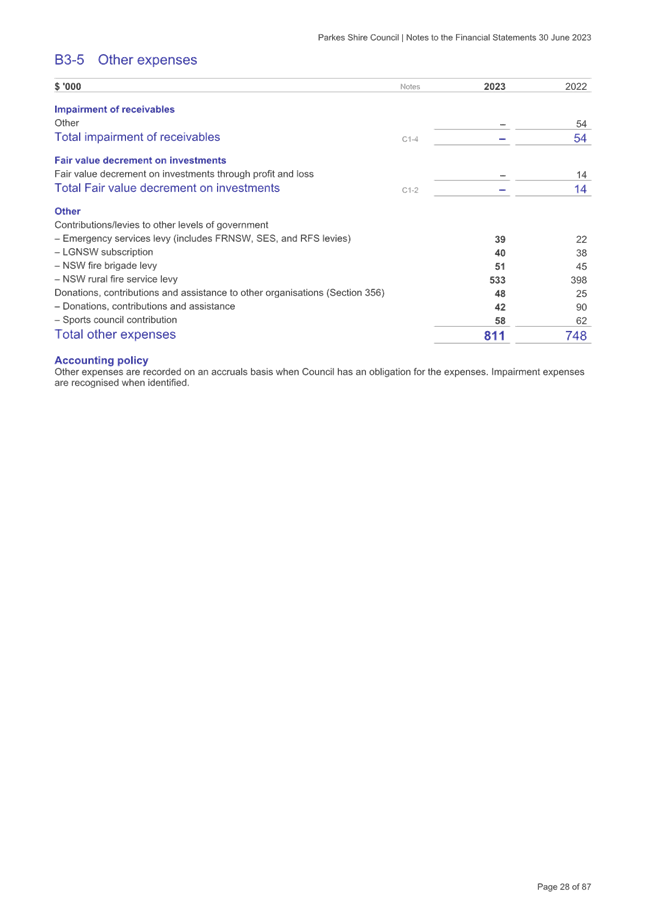

·

The Committee queried the following

in relation to B3-5 Other Expenses:

o

Increase in receivables for the 2023

financial year. The Financial Accountant advised that this relates to the

income accrual from Transport for NSW for outstanding storm damage funding

not yet received by council at YE.

o

Council's Financial Accountant raised

the significant work undertaken by Council's Rates team to reduce doubtful

debts equalling $33,000.

·

The Committee identified a

transposition error on page 54 of the Business Paper under Capital grants and

contributions. Council's Financial Accountant advised that this error has

been amended.

·

The Committee queried if Council has

received communication from Ministers regarding the Rural Fire Service

funding. The General Manager advised that he and the Mayor met with Ministers

in Sydney and that it seems unlikely that changes will be made to the Rural

Fire Services Act 1994 (NSW) in relation to equipment purchases.

·

The Committee queried why there are

no graphic to visually represent performance measure ratios and explanation

of risks. The Chief Financial Officer advised that the graphics are provided

in the final Financial Statements.

·

The Committee queried if Council

utilises other measures or metrics to identify problems that could be

presented to the Audit, Risk and Improvement Committee. The Chief Financial

Officer advised that Council prepares monthly reports to Council as well as

Directors to track progress against the budget.

·

The Committee commended the Finance

Team on their great work with this report.

|

|

Resolved

ARIC 037/23

That the Audit, Risk and

Improvement Committee:

1. Receive

and note the Audited Financial Statements for the year ended 30 June 2023

.Carried

|

8 Report

of Confidential Resolutions

Nil

9 Conclusion

of Meeting

The meeting concluded at 10.00am.

This is the final page of the minutes comprising 6 pages

numbered 1 to 6 of the Audit, Risk and Improvement Committee Meeting held on Wednesday,

30 August 2023 and confirmed on Friday, 13 October 2023.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

5 Disclosures

of Interests

All Council Officials must disclose

and manage any conflicts of interest they may have in matters being considered

at the meeting.

Council's Code of Conduct deals with pecuniary and

non-pecuniary conflicts of interest and political donations, and provides

guidance on how these issues should be managed.

Council Officials must be

familiar with Council's Code of Conduct and their obligations to disclose and

manage any conflicts of interest that they may have in matters being considered

at this Council Meeting.

Note: Council Officials who declare an Interest at

the Meeting are also required to complete a Declaration of Interest form.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

6 Late

Business

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

7 Officers'

Reports

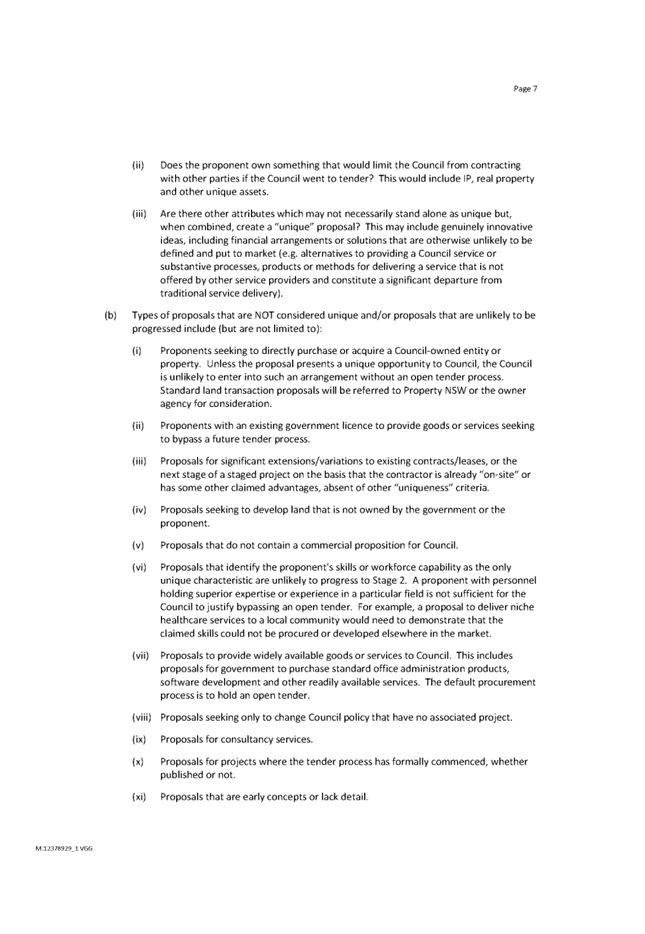

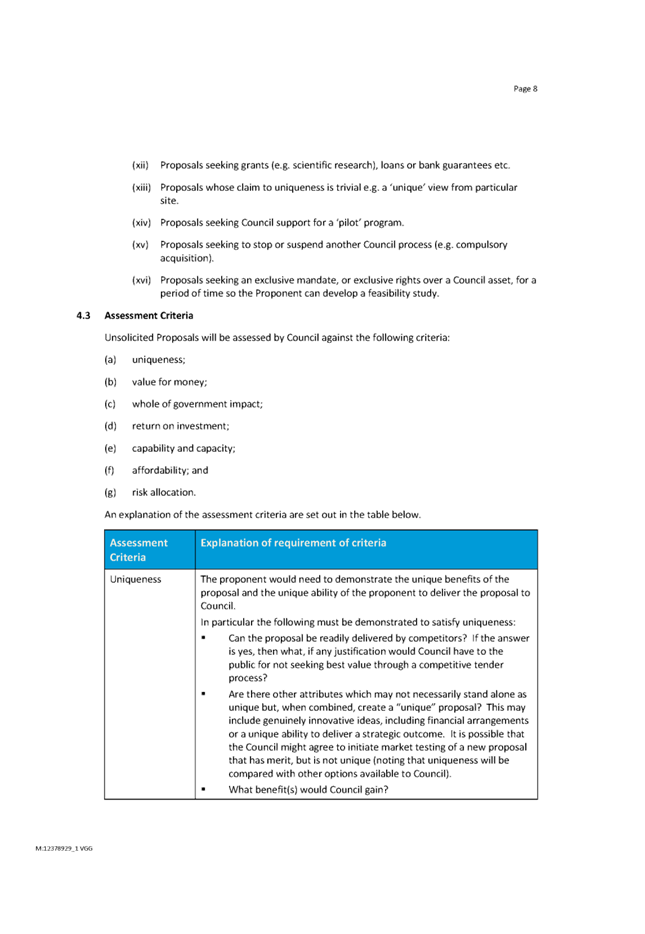

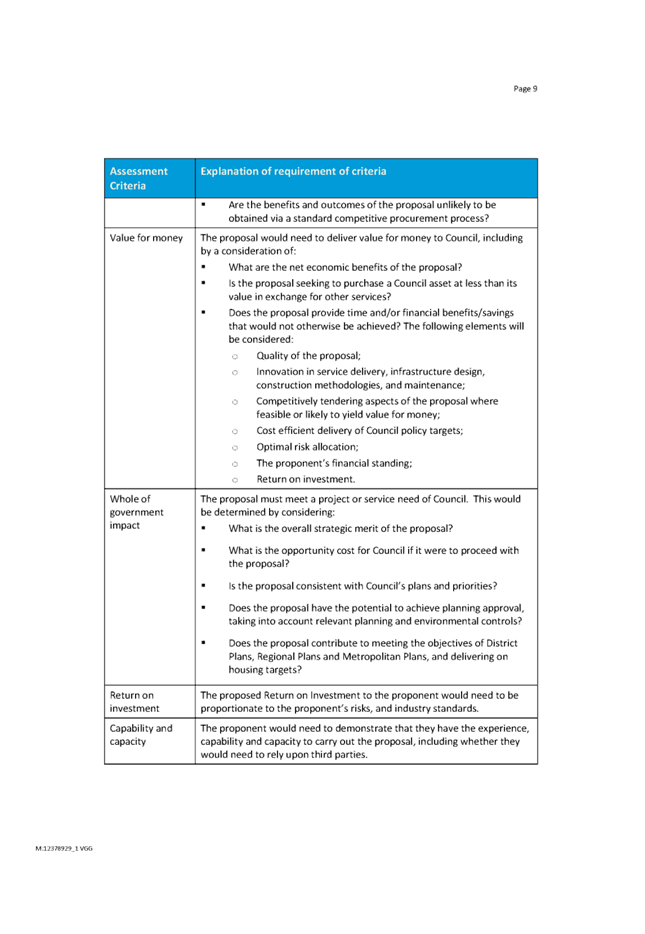

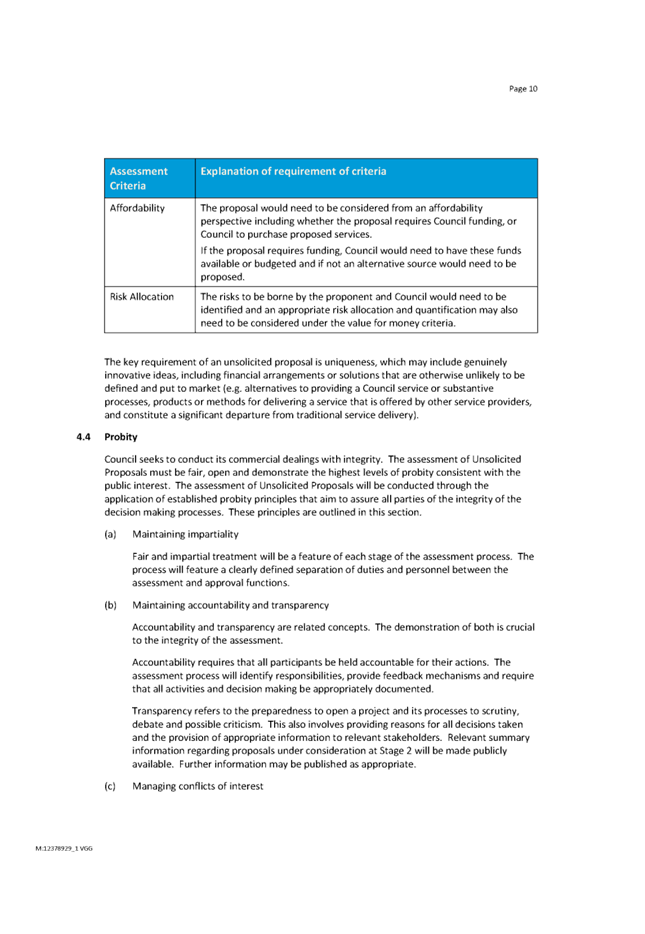

7.1 Unsolicited

Bid Policy and Procedure

IP&R Linkage: Pillar:

Leadership

Goal: Our local government

is open, accountable, and representative.

Strategy: Provide open and

transparent decision-making and undertake the civic duties of Council with

professionalism and integrity.

Author: Kent

Boyd PSM, General Manager

Authoriser: Kent

Boyd PSM, General Manager

Annexures: A. Unsolicited

Bid Policy - Original

|

Recommendation

That the Audit, Risk and Improvement Committee:

1. The

Committee note the role of ARIC as an oversight body in the Unsolicited Bid

Policy and endorsed its tabling at a Council meeting in due course.

|

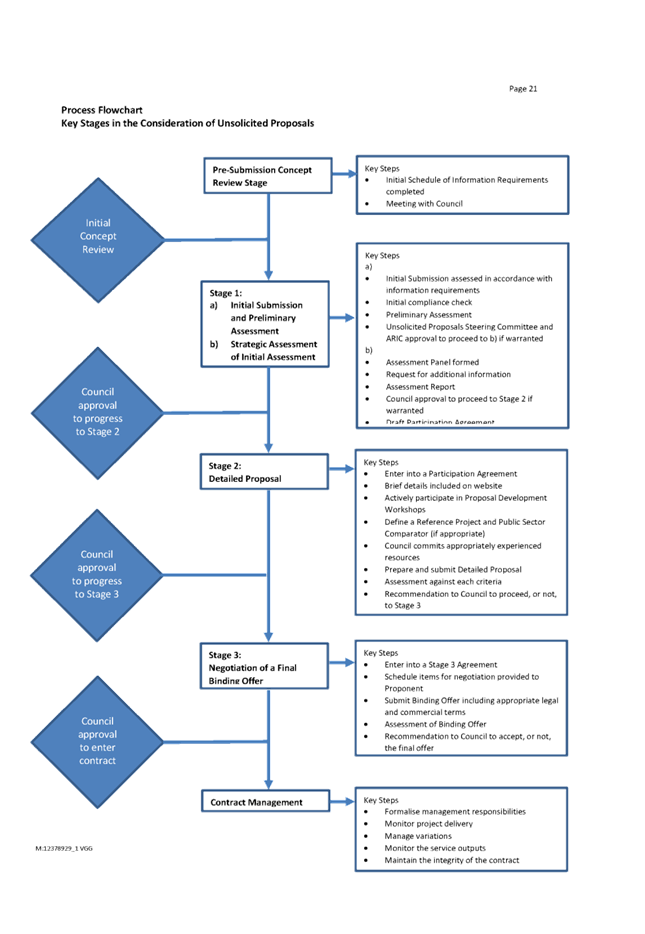

Background

An important component of Council's corporate governance

responsibility is the progressive development and review of Council's policies.

Council from time to time receives unsolicited approaches

for products, services and joint ventures and expects to receive an increase

unsolicited proposal into the future.

An Unsolicited Bid Policy and Procedure was approved at the

Council meeting held on 16 February 2021, which is attached. The current ARIC

was not formed at that time and accordingly did not have input on the Policy

and Procedures but is significantly involved in the process. Accordingly, the

Policy and Procedure is presented for the ARIC's review.

It is anticipated to be presented to Council at the 17

October 2023 Council meeting, then if approved put out for public consultation.

ISSUES AND COMMENTARY

Council from time to time receives unsolicited approaches

for products, services and joint ventures and expects to receive an increase

number of unsolicited proposal into the future catalysed by the Parkes Special

Activation Precinct.

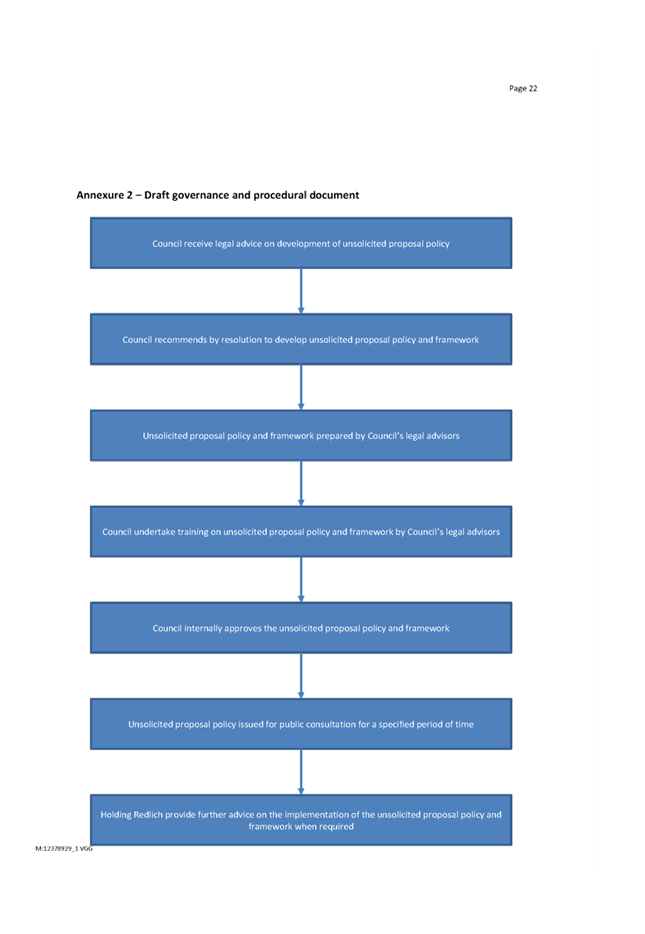

Legal advice was previously sought from Holding Redlich

(solicitors) in relation to the unsolicited proposals described above. Holding

Redlich advised Council that it is able to consider an unsolicited proposal if

it has in place an unsolicited proposal policy that is consistent with the

requirements of the Local Government Act 1993 (NSW) (Act) and the NSW

Government Unsolicited Proposals: Guide for Submission and Assessment dated

August 2017 (Unsolicited Proposals Guidelines).

Holding Redlich advised on other avenues to consider the

unsolicited proposal including a tender exemption under s 55 of the Act, a

public private partnership (PPP) under Chapter 12, Part 6 of the Act and

alternative commercial structures. They advised Council that developing and

adopting an unsolicited proposal policy was the most appropriate

solution.

There is evidence of other Council’s developing such

policies: Central Coast Council (2019 - draft form for public consultation),

Wollongong Shire Council (2018 - draft form for public consultation) and City

of Marion (SA) (2018 - adopted under s49 of the Local Government Act 1999 (SA).

This would also allow Council to efficiently consider further unsolicited

proposals in the future and be a leader in innovative procurement and project

development.

A full copy of Holding Redlich’s advice is provided

for information.

The draft Unsolicited Proposal Policy and procedure was

tabled at the 08 December 2020 meeting of the Council's Audit Risk and

Improvement Committee (ARIC) for comment. The Committee noted the

inclusion of ARIC as an oversight body in the draft Policy and endorsed its

tabling at a Council meeting in due course.

Legislative and Policy Context

Local Government Act 1993 (NSW) (Act) and the NSW Government

Unsolicited Proposals: Guide for Submission and Assessment dated August 2017

(Unsolicited Proposals Guidelines).

Financial Implications

There is no financial implications arising from this policy,

other than advertising costs and some training costs.

Risk Implications

There are inherent risks with direct dealings. The

Unsolicited Bid Policy seeks to minimise the risk using the appropriate

Policy/Procedure framework.

Community Consultation

It is intended to advertise the policy if ARIC and Council

agree.

Conclusion

The Unsolicited Bid Policy and Procedure provides a risk

based framework for Council to manage unsolicited approaches for products,

services and joint ventures.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

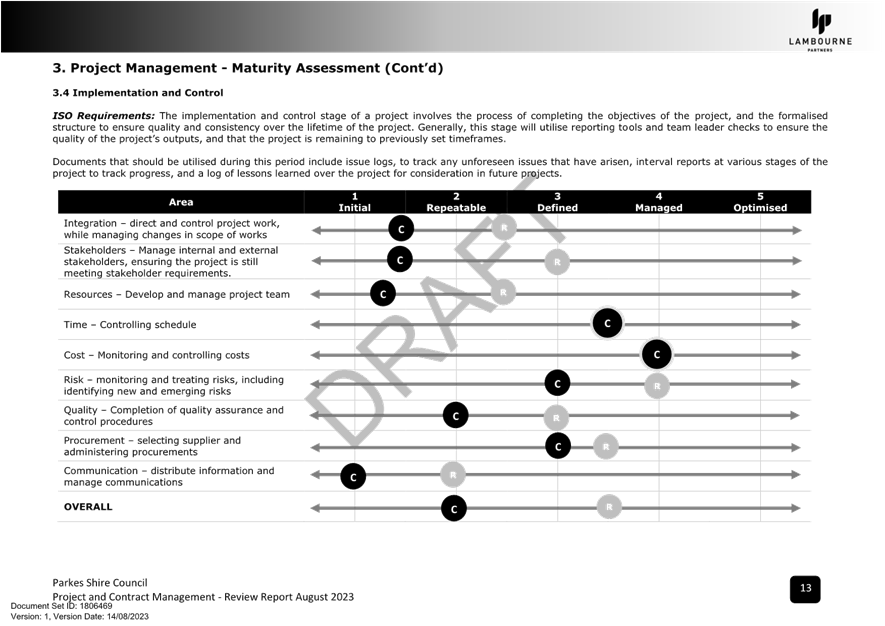

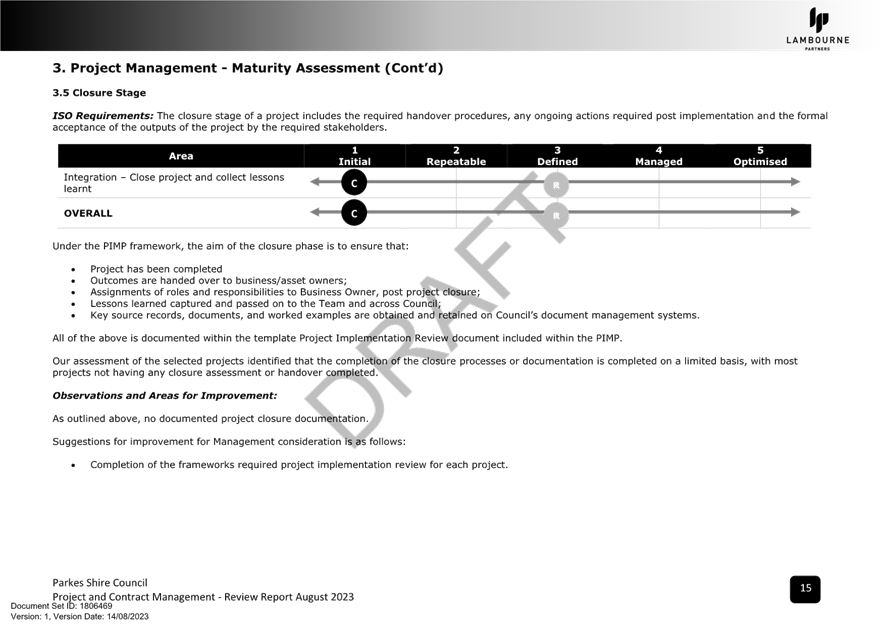

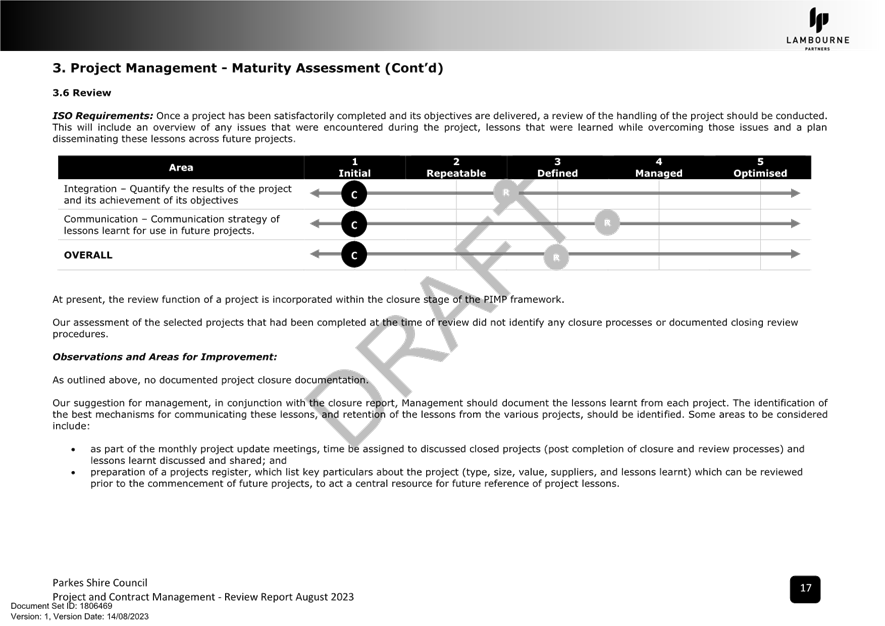

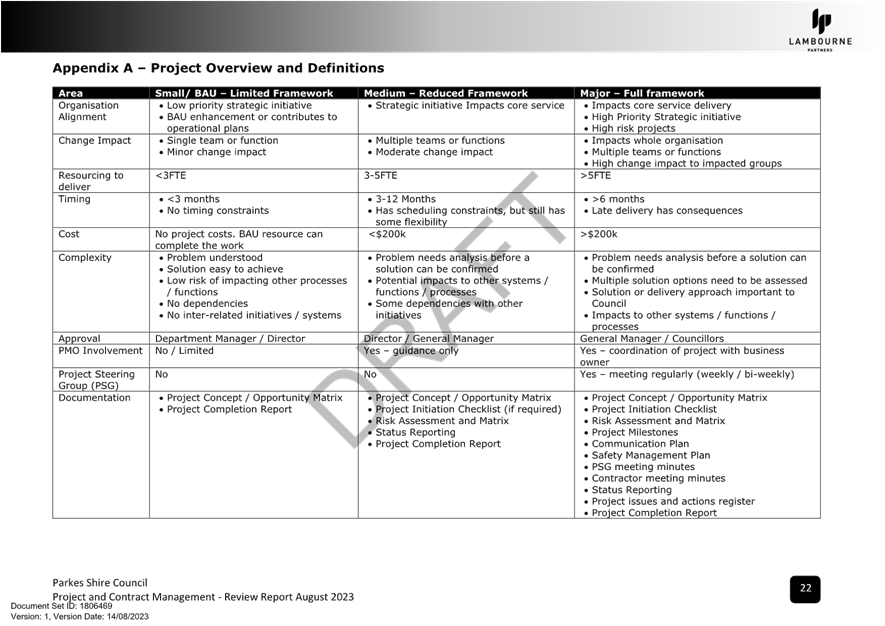

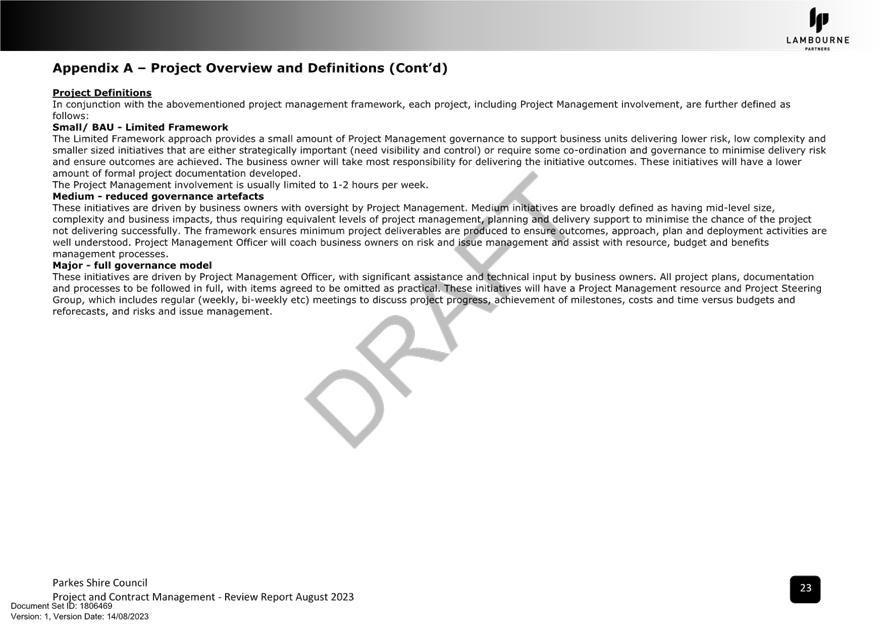

7.2 Internal

Audit - Project Management Maturity Assessment

Author: Mikaela

Cass, Manager Governance, Risk and Corporate Performance

Authoriser: Carrie

Olsen, Executive Manager Economy, Destination and Activation

Annexures: A. Draft

Project Management Maturity Assessment Report - Lambourne Partners

|

Recommendation

That the Audit, Risk and Improvement Committee:

1. Receive

and note the Project Management Maturity Assessment Report and presentation

by Lambourne Partners.

|

SECTION 428A RESPONSIBILITY

The Section 428A Responsibility associated with this report,

as detailed in the Section 428A (2) of the Local Government Act 1993, is:

(a) compliance

Background

Council Officers commenced work with

Lambourne Partners to undertake a maturity assessment of Council's Project

Management framework against the Australian Standard ISO 21500:2020 Project,

programme, and portfolio management — Guidance on project management.

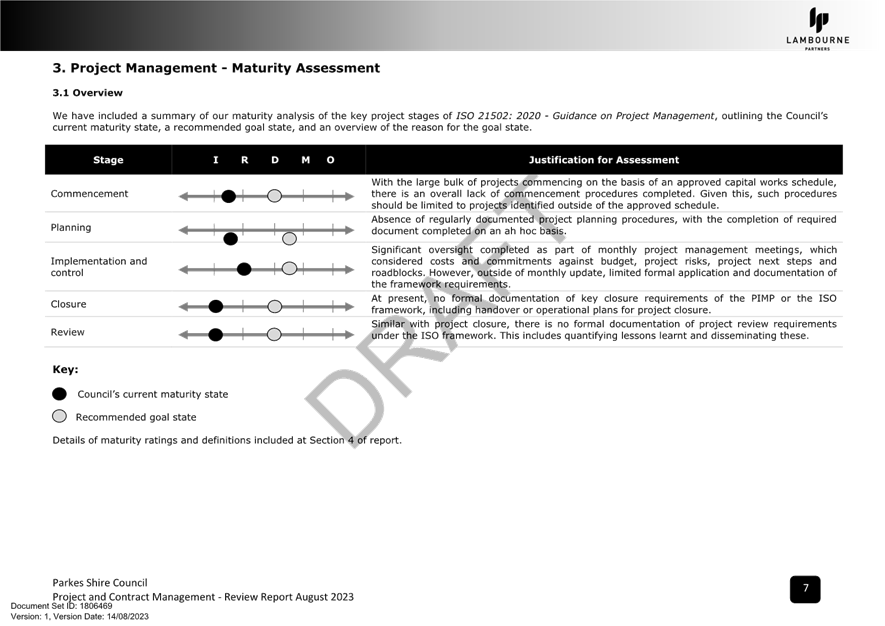

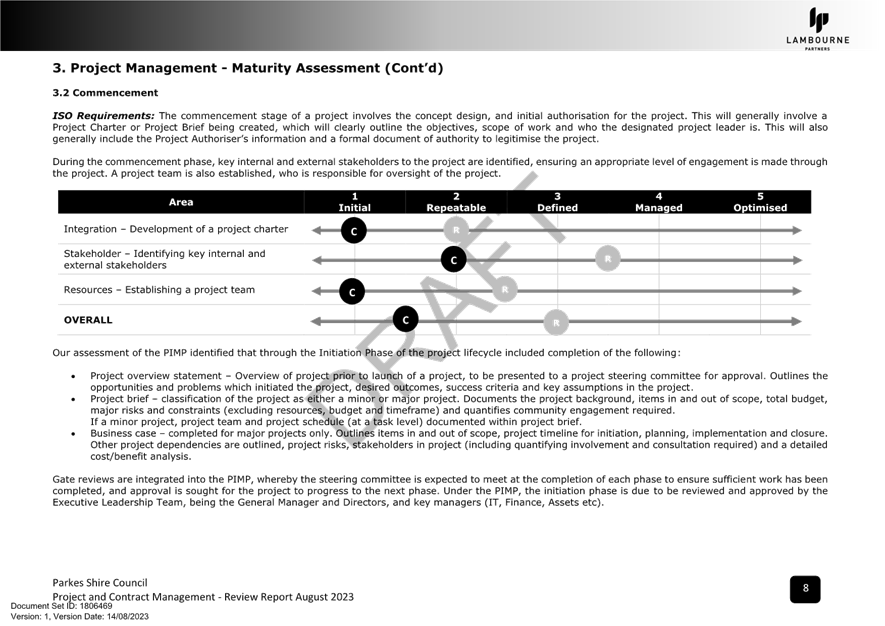

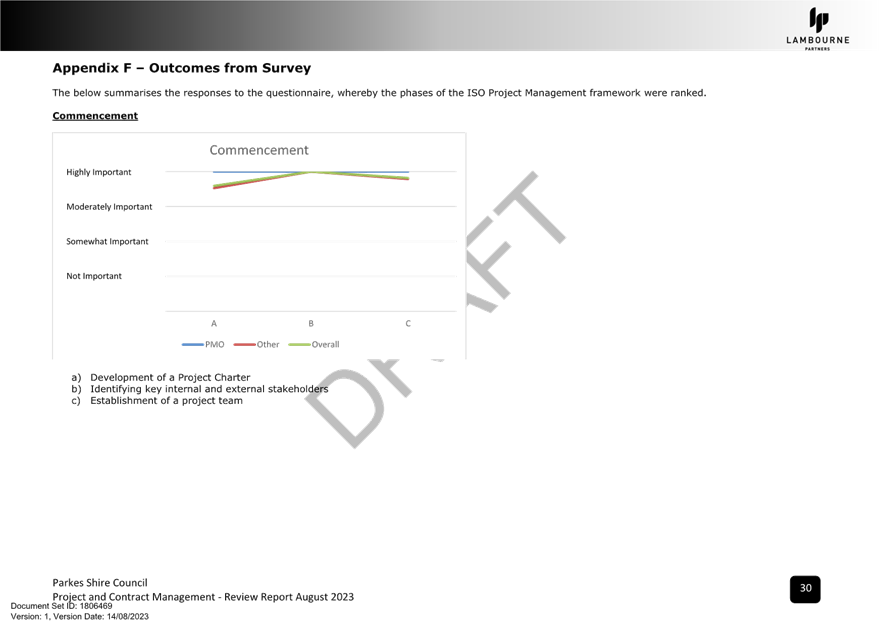

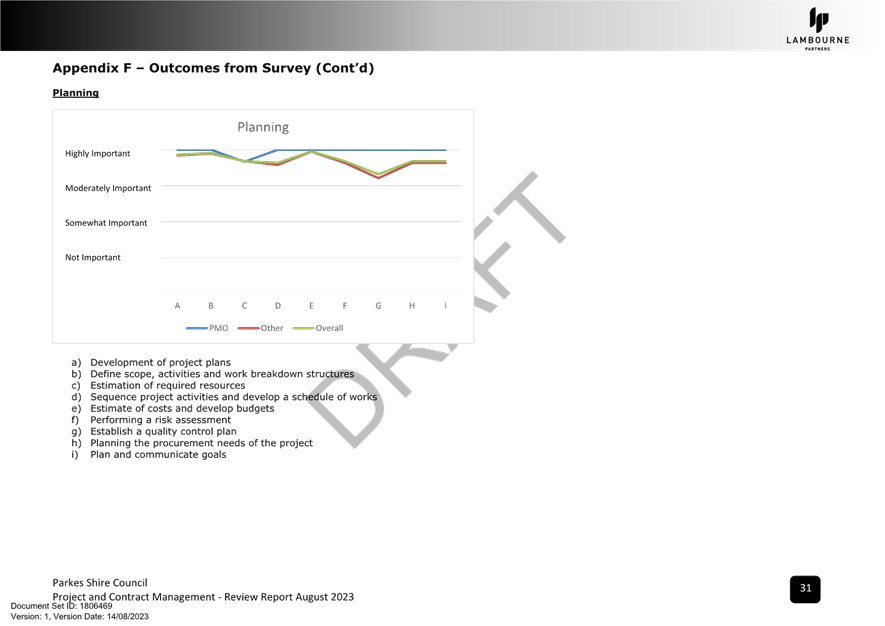

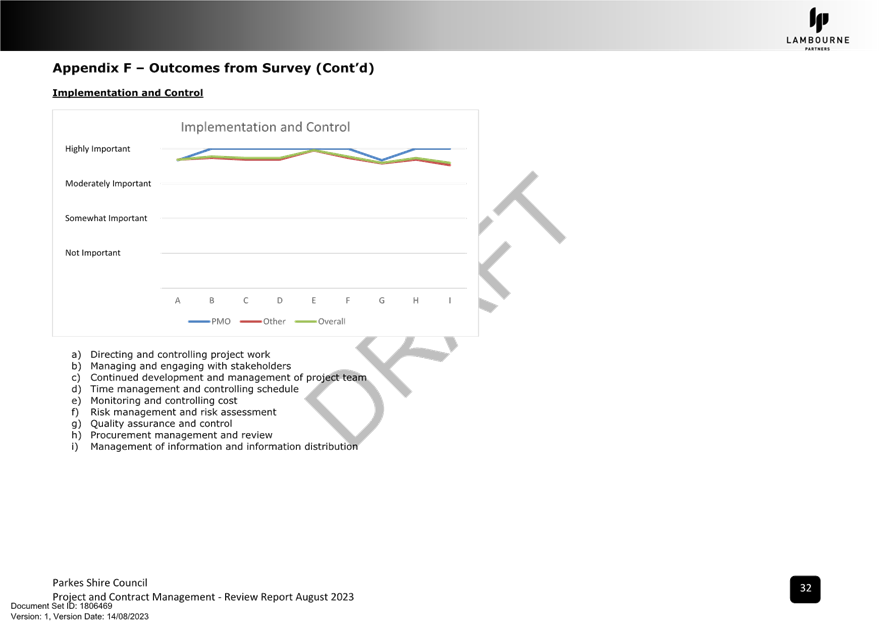

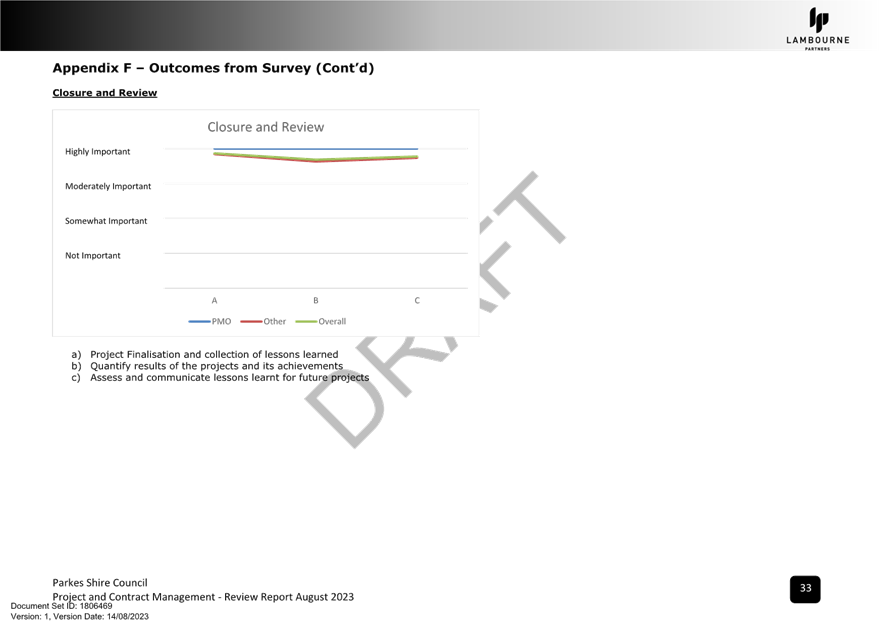

The maturity assessment includes a review of:

· the overall

project management framework at Council;

· quantification of

Management expectations with regards to the Council’s project management

methodology regarding the following aspects of project management:

o commencement;

o planning;

o implementation and control;

o closure; and

o review;

· for a sample of

Council projects, understand the existence and effectiveness of any procedures,

practices and templates utilised by Council in the management of projects.

Current practices to be considered to identify any repeatable practices and

robust templates and forms which could be retained in any maturity actions.

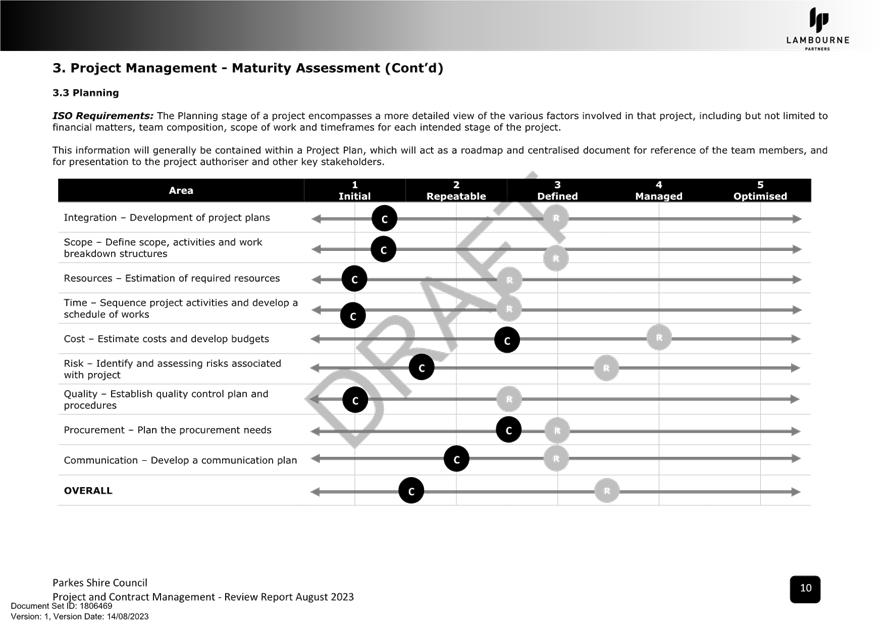

ISSUES AND COMMENTARY

Paul Quealey,

Partner, Audit and Assurance at Lambourne Partners was on-site in June 2023 and

met with a number of key stakeholders to discuss Council's existing Project

Management framework.

The outcomes

from the meetings between Lambourne and Council Officers and a review of source

records identified that project management at Council is completed under two

clear frameworks. These frameworks are as follows:

· Project Management

Office; and

· Asset and

Operational departments of Council.

Paul will be

in attendance to present the findings of the Project Management Maturity

Assessment to the ARIC, with the key audit findings being that the project

methodologies applied under the above areas of Council are extremely separate

and distinct, and are summarised as follows:

Project

Management Office

Highly formalised and structured project management methodology, which is

utilised by dedicated and experienced project management employees in the

execution of large value, complex and strategically important infrastructure

projects for the Parkes Shire and State and Federal Governments. The resources

within the office are dedicated and experienced project management personnel.

The office is

subject to a high level of key management oversight (Director and General

Manager), with regular project management meetings and updates on progress and

risk management.

Asset and

Operational departments of Council

Assets, engineering and operational departments operate under a Project

Implementation & Management Program (PIMP). The PIMP was developed by the

City of Ryde Council, and acquired in 2013 to be the overarching project

management framework and methodology. The PIMP includes the following key

areas:

· Defining project

lifecycle;

· Procedures for the

management of the project lifecycle, including initiation, planning,

implementation, and closure.

· Workpaper and form

templates, and "how to" guides to complete various project

documentation.

Lambourne's

assessment concluded on the maturity of each framework as follows:

· Project

Management Office - Project management framework is considered Managed. The

project management office has a well-defined, structured and risk focused

project management approach. The framework is designed to be agile around the

individual project requirements, expectations and needs. This was evident with

the current Water Security Program, which has a specially designed procurement

plan and approach, to ensure value for money is achieved and purchasing and

supplier risks are mitigated.

· Asset and

Operational departments - The project management framework for the

remaining areas of Council is considered initial to repeatable. A defined

framework exists, however the utilisation of this framework is not consistent,

nor is there consistent completion and retention of key project management

documentation. Projects are closely tracked, particularly by Finance, however

limited to no evidence of consistent adherence with the PIMP.

A detailed

Action Plan, including six distinct actions, was proposed by Lambourne and

endorsed by Council's Executive Leadership Team (ELT) in September 2023. These

actions will be assigned to the appropriate Council Officers and tracked

accordingly, before being reported back to the ARIC.

Legislative and Policy Context

Office

of Local Government's Risk Management and Internal Audit Guidelines for Local

Government in NSW (November 2022)

Financial Implications

The estimated costs for the Project Management Maturity

Assessment are $6,900 including travel and out of pocket expenses. These costs

will be funded from Council's Internal Audit budget.

Risk Implications

Council’s internal audit function assists Council in

achieving its objectives by bringing a systemic disciplined approach to

evaluating and improving the effectiveness of risk management, control, and

governance processes. There are no major risks associated with the conduct of

the Assessment.

Community Consultation

There are no community consultation requirements for Council

associated with this report.

Conclusion

Paul Quealey,

Partner, Audit and Assurance at Lambourne Partners was on-site in June 2023 and

met with a number of key stakeholders to discuss Council's existing Project

Management framework.

The outcomes

from the meetings between Lambourne and Council Officers and a review of source

records identified that project management at Council is completed under two

clear frameworks.

A detailed

Action Plan, including six distinct actions, was proposed by Lambourne and

endorsed by Council's Executive Leadership Team (ELT) in September 2023.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

7.3 Improvement

- Draft 2022-23 Annual Report

Author: Mikaela

Cass, Manager Governance, Risk and Corporate Performance

Authoriser: Carrie

Olsen, Executive Manager Economy, Destination and Activation

Annexures: A. 2022.23

Annual Report (DRAFT) ⇩

B. Parkes

Shire Council Annual Financial Statements 30 June 2023 ⇩

|

Recommendation

That the Audit, Risk and Improvement Committee:

1. Review

and provide feedback on the draft 2022-23 Annual Report prior to adoption at

Council's November Ordinary Meeting.

|

SECTION 428A RESPONSIBILITY

The Section 428A Responsibility associated with this report,

as detailed in the Section 428A (2) of the Local Government Act 1993, is:

(a) compliance

(f) implementation of the strategic plan, delivery program and strategies

ISSUES AND COMMENTARY

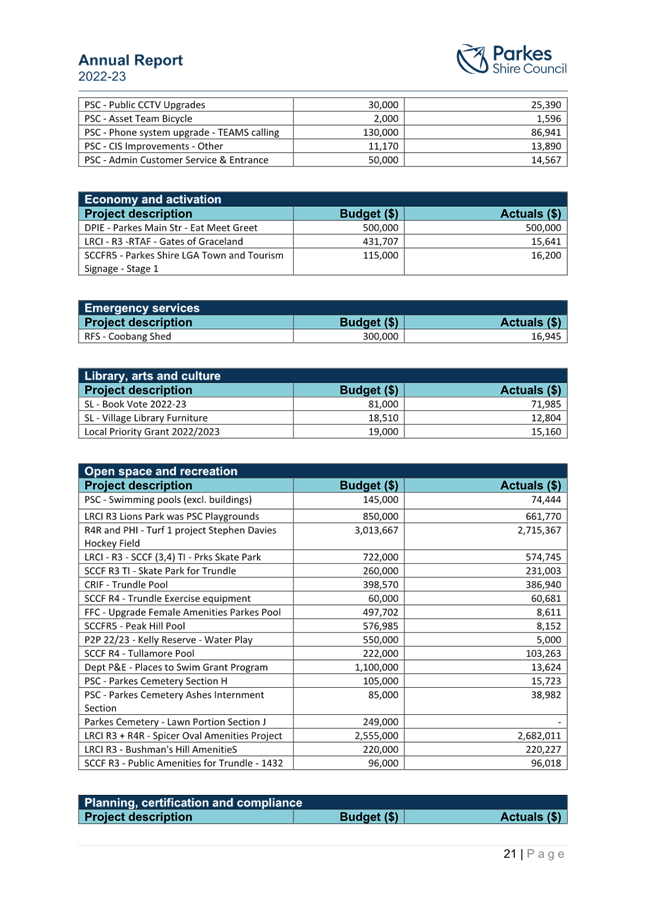

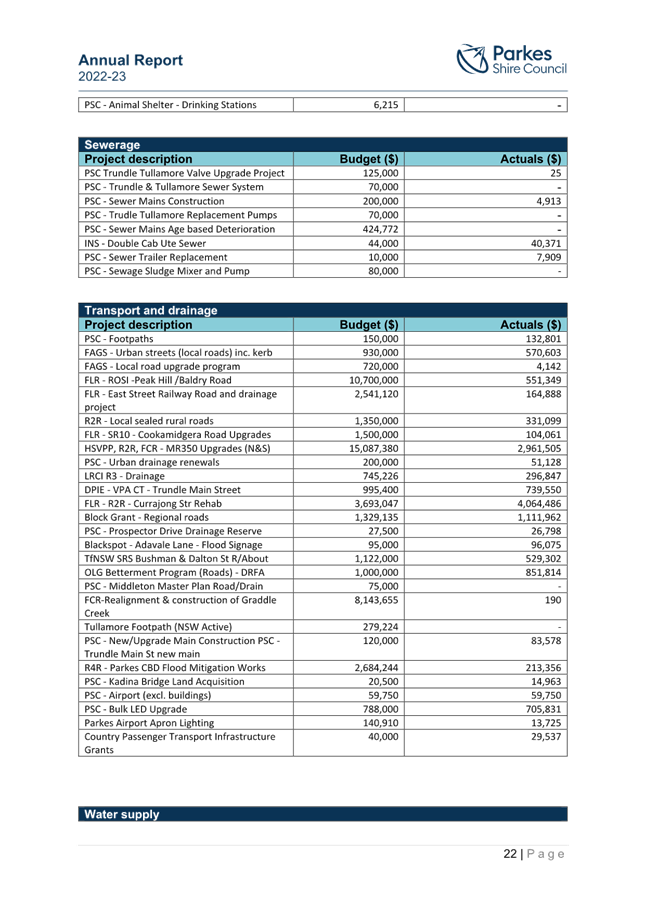

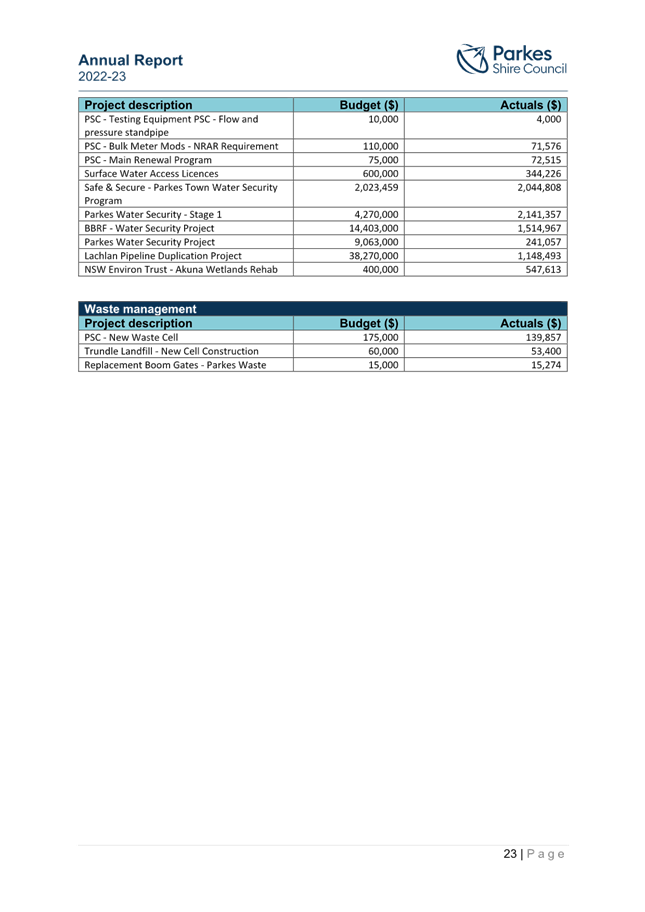

The draft Annual Report, appended at Annexure 1,

summarises Council’s performance over the 2022-23 year and highlights the

projects, services, programs and events delivered during the reporting period

to support the implementation of Council’s Delivery Program 2017-2022 and

Operational Plan 2022-23.

The draft Annual Report also contains information on several

other statutory and regulatory matters, including Council’s financial

performance for the reporting period. The Annual Report comprises the following

sections:

· Part 1 -

Introduction: Includes a message from the Mayor and General Manager and

outlines the IP&R framework, including the role and purpose of the Annual

Report, and provides an overview of Council, including Councillors, Council

meetings and committees, and its organisation structure during the 2022-23

reporting period.

· Part 2 -

2022-23 Year in Review: Reports on the financial performance of Council's

2022-2023 Operational Plan, including Council's Capital Works Program for the

2022-23 reporting period, as required under the Capital Expenditure Guidelines

issued by the OLG pursuant to section 23A of the Act.

· Part 3 -

Achieving our Operational Plan: Reports on Council’s progress in

implementing its 2022-23 Operational Plan.

· Part 4 -

Statutory Reporting: Reports on Council’s general reporting

requirements set out in section 428 of the Act and clause 217 of the

Regulation, as well as other reporting requirements imposed on Council by other

legislation.

· Appendix A -

Government Information (Public Access) Act Reporting: Contains

Council’s Government Information (Public Access) Act 2009 Annual Report

for the 2022-23 reporting period.

· Annexures B -

Audited Financial Statements: Contains Council’s audited Financial

Statements for the Year Ended 30 June 2023 and Independent Auditor’s

Report.

A copy of Council's 2022-23 Annual Report is provided for

review of the Audit, Risk and Improvement Committee. Feedback is invited and

will be considered before the 2022-23 Annual Report is tabled at Council's

November Ordinary Meeting for adoption.

Legislative and Policy Context

The Integrated Planning and Reporting (IP&R) provisions

of the Local Government Act 1993 (the Act) require Parkes Shire Council

(Council) to prepare an Annual Report detailing its achievements in

implementing its adopted Delivery Program and Operational Plan over the

previous financial year.

Financial Implications

There are no financial implications for the Audit, Risk and

Improvement Committee to consider with respect to this report, however, the

Annual Report does present a summary of Council’s performance over the

2022-23 financial year and as required under the Regulation, contains a copy of

the organisation’s audited Financial Statements for the 2022-23 year.

Risk Implications

Adoption of the 2022-23 Annual Report ensures Council

complies with its legislative requirements under section 98 of the Act.

Conclusion

A copy of Council's 2022-23 Annual Report is provided for

review of the Audit, Risk and Improvement Committee. Feedback is invited and

will be considered before the 2022-23 Annual Report is tabled at Council's

November Ordinary Meeting for adoption.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

7.4 Improvement

- Information Asset Register

Author: Bianca

Hinton, Records and Information Management Coordinator

Authoriser: Carrie

Olsen, Executive Manager Economy, Destination and Activation

Annexures: A. Information

Asset Register (draft) ⇩

|

Recommendation

That the Audit, Risk and Improvement Committee:

1. Provide feedback

on the current state and next steps of Council's draft Information Asset

Register.

|

SECTION 428A RESPONSIBILITY

The Section 428A Responsibility associated with this report,

as detailed in the Section 428A (2) of the Local Government Act 1993, is:

(a) compliance

(e) governance

ISSUES AND COMMENTARY

Council engaged Record Keeping Innovation (RKI) in May 2023

to undertake the current state assessment and identify opportunities for

improvement. A key deliverable of the current state assessment included the

development of an Information Asset Register (IAR) that:

· Defines

information assets

· Identifies

custodians of information assets

· Identifies owners

of systems

· Established a risk

profile for information assets

· Identifies

recordkeeping retention requirements

· Established

responsibilities of information asset owners

RKI and Council's Records and Information Management team

have commenced the development of a draft IAR to be used as a key corporate

tool for managing high value/high risk information, data and records and will

be present at the meeting to discuss the current state and next steps. A copy

has been provided for the information of the Committee and is appended at Annexure

A.

Legislative and Policy Context

The Information Asset Register ensures compliance with

Council's Information Management Framework and the National Archives of

Australia's "Building

trust in the public record: managing information and data for government and

community" policy which identifies key requirements for

managing Australian Government information assets (records, information and

data) to help agencies improve how they create, collect, manage and are able to

use information assets.

Financial Implications

There are no financial implications for the Audit, Risk and

Improvement Committee to consider with respect to this report.

Risk Implications

The Current State Assessment Report identified the IAR as a High

risk. An IAR will help to identify and control Council's information assets. The

register will focus on high value information and should identify all

information assets including digital and hardcopy, the systems they are managed

in (current and legacy) and should highlight possible risks to the records

managed within the systems. Managing information assets in this way will help avoid

the risk of data loss in the future and identifying information assets in an

information asset register, will ensure records are identified and can be

managed according to their value on an ongoing basis.

Conclusion

Council's Records and Information Management team have

commenced the development of a draft IAR. A copy has been provided for the

information of the Committee and is appended as Annexure A.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

7.5 Risk

Management - Insurance Portfolio Review

Author: Nikki

Bevan, Procurement and Contracts Specialist

Authoriser: Carrie

Olsen, Executive Manager Economy, Destination and Activation

Annexures: A. Civic

Risk Mutual Memo on Contiributions ⇩

B. Council

Insurance Policies ⇩

|

Recommendation

That the Audit, Risk and Improvement Committee:

1. Note the Insurance

as complying with Legislation and reducing risk.

|

SECTION 428A RESPONSIBILITY

The Section 428A Responsibility associated with this report,

as detailed in the Section 428A (2) of the Local Government Act 1993, is:

(b) risk management

ISSUES AND COMMENTARY

Parkes Shire Council is required by Legislation to acquire

adequate Public Liability Insurance.

Parkes Shire Council are a member of Civic Risk Mutual, a

company limited by guarantee, which is both an unregistered managed investment

scheme and a discretionary mutual fund. A mutual discretionary fund is a scheme

where Members contribute money which is pooled for the purposes of acquiring

general insurance products and protections to cover the specified risks of the

Members and for paying claims by Members, on a discretionary basis, up to a

certain specified limit.

The purpose of participating in Civic Risk Mutual Limited is

to participate in a range of Membership Benefits including risk protection and

risk management support. The purpose of participation is not to make an

investment or receive a return on the investment of money.

Legislative and Policy Context

Local

Government Act 1993 Part 4

A council must

make arrangements for its adequate insurance against

public liability and professional liability.

Financial Implications

The overall increase for Parkes Shire Council is +$49,000 or

+7 % from $744,010 in 2023 to $794,010 in 2024 which is driven by insurance

market increases in property and cyber (driven by national claims) and our

member surplus rebuilding strategy. Parkes Shire Council was also impacted by

increased property claims and an increase in insurable assets. This is before

any profit share is known and allocated which is tracking strongly in 22/23 to

date.

Risk Implications

Having inadequate insurance or no insurance at all, creates

a high risk to council. Council may be required to pay for repairs or

replacement of Assets and provide payments to external sources in cases or

incident, injury and damage.

Adequate insurance is a requirement by legislation and lack

of insurance could affect current and future grants and funding resulting in

financial implications.

Conclusion

Council has undertaken adequate insurance to minimise risk

factors and comply with legislation.

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

8 Confidential

Matters

|

Recommendation

That Audit, Risk and Improvement Committee:

1. Moves into Closed

Session to deal with the matters below, which are classified as confidential

under section 10A(2) of the Local Government Act 1993 for the reasons

specified:

8.1 Future

Parkes Residential Land Proposal - Confidential

This matter is considered to be

confidential under Section 10A(2) - c of the Local Government Act, and the

Council is satisfied that discussion of this matter in an open meeting would,

on balance, be contrary to the public interest as it deals with information

that would, if disclosed, confer a commercial advantage on a person with whom

the Council is conducting (or proposes to conduct) business.

Further it is considered that

discussions of this matter in open Council would, on balance, be contrary to

the public interest as it would prejudice Council's ability to secure the

optimum outcome for the community.

8.2 General

Managers Report to ARIC - October 2023

This matter is considered to be

confidential under Section 10A(2) - d(i) of the Local Government Act, and the

Council is satisfied that discussion of this matter in an open meeting would,

on balance, be contrary to the public interest as it deals with commercial

information of a confidential nature that would, if disclosed prejudice the

commercial position of the person who supplied it.

Further it is considered that

discussions of this matter in open Council would, on balance, be contrary to

the public interest as it would prejudice Council's ability to secure the

optimum outcome for the community.

2. Exclude the media

and public from the meeting on the basis that the business to be considered

is classified as confidential, pursuant to 10A(1), 10(2) and 10A(3) of the Local

Government Act 1993.

3. Withhold reports

and correspondence relevant to the subject business be withheld from the

media and public as provided by section 11(2) of the Local Government Act

1993.

4. Make public

resolutions made by the Council in Closed Session after the conclusion of the

Closed Session, and record such resolutions in the minutes of the Council

meeting.

Background, Issues and Commentary

In accordance with section 10A(2) of the Local

Government Act 1993, Council may close part of its meeting to deal with

business of the following kind:

(a) Personnel matters

concerning particular individuals (other than councillors).

(b) Personal hardship of

any resident or ratepayer.

(c) Information that

would, if disclosed, confer a commercial advantage on a person with whom

Council is conducting (or proposes to conduct) business.

(d) Commercial

information of a confidential nature that would, if disclosed:

(i) Prejudice the

commercial position of a person who supplied it: or

(ii) Confer a commercial

advantage on a competitor of Council;

(iii) Reveal a trade

secret.

(e) Information that

would, if disclosed, prejudice the maintenance of law.

(f) Matters

affecting the security of Council, Councillors, Council staff and Council

property.

(g) Advice concerning

litigation, or advice that would otherwise be privileged from production in

legal proceedings on the grounds of legal professional privilege.

(h) Information

concerning the nature and location of a place or an item of Aboriginal

significance on community land.

(i) Alleged

contraventions of any Code of Conduct requirements applicable under section

440.

It is my opinion that the

business listed in the recommendation is of a kind referred to in section

10A(2) of the Local Government Act 1993 and, under the provisions of

the Act and the Local Government (General) Regulation 2021, should be

dealt with in a part of the meeting that is closed to members of the public

and the media.

Pursuant to section 10A(4) of

the Act and clauses 14.9–14.10 of Council's Code of Meeting Practice,

members of the public may make representations to the meeting immediately

after the motion to close part of the meeting is moved and seconded, as to

whether that part of the meeting should be closed.

|

|

Audit,

Risk and Improvement Committee Meeting Agenda

13

October 2023

|

9 Report

of Confidential Resolutions

In accordance with clauses

14.22 and 14.23 of Council's Code of Meeting Practice, resolutions passed

during a meeting, or a part of a meeting that is closed to the public must be

made public by the Chairperson as soon as practicable. Such resolutions

must be recorded in the publicly available minutes of the meeting.